From the Desk of Nick Crow, CFA

President, Motley Fool Wealth Management

Dear Fellow Fool,

If there’s one thing I realized in my prior career as an investment analyst for The Motley Fool, it’s that humans are simply not genetically predisposed to being good investors.

Now, everybody knows we’re rash, impulsive, and prone to taking action just for the sake of doing so. But in actuality, our problems as investors run far deeper than that, as you’ll see in a minute. And when we don’t stop and take the time to distinctly identify them, we’re only encouraging ourselves to repeat them over and over… costing us a pretty penny in the process!

So when I learned that my good friend and former colleague Morgan Housel — whom you likely know from his nationally syndicated financial articles with both The Motley Fool and The Wall Street Journal — was researching this very issue and had actually isolated six potentially devastating portfolio mistakes that even the most grizzled of Wall Street veterans make regularly (though you won’t hear them say it), I knew I had to share his eye-opening article below with Fools like you.

Here’s why. Roughly two years ago, Motley Fool co-founder and CEO Tom Gardner personally asked me to help found and serve as president of Motley Fool Wealth Management — a sister company of The Motley Fool that you might have heard of that provides members with a unique and Foolish twist on money management.

And one of the primary reasons I leapt at the chance to accept Tom’s offer was the opportunity to not just tell Fools over and over again (like I used to do as an analyst in Motley Fool Pro) about the vital importance of traditional Foolish philosophy like having the patience and fortitude to weather volatility over the long term… not trying to time the stock market’s ups and downs… and not selling your winning stocks too early when they still have great business models…

But to actually handle all of those knee-jerk decisions for them in Motley Fool Wealth Management — thereby taking emotion 100% out of the decision-making process.

Not to mention saving time-strapped Fools just like you the hours, or even days, of exhaustive research and thought that go into every buying… selling… and rebalancing decision you make.

That said, what I’m actually proudest of as the president of Motley Fool Wealth Management is that as a Registered Investment Advisor, Fool Wealth actually has a legal obligation (known as a “fiduciary standard” in the financial world) to always provide you with financial advice that is in YOUR best interest.

For these reasons and more, I urge you to take just a few minutes out of your day to peruse Morgan’s enlightening report below. I think you’ll find it well worth your while to see how Motley Fool Wealth Management could immediately alleviate the six wealth-devastating portfolio mistakes he recently identified (many of which you may be making yourself right this minute… without even knowing it) — by making each and every one of your portfolio decisions for you.

And after you do so, please feel free to explore the rest of our Fool Wealth home page to see whether this innovative wealth management solution may be right for you. If it is, I invite you to join us in Motley Fool Wealth Management over the next few weeks (please note, we’re already accepting new clients as we speak!).

A quick word of warning, though… to make 100% certain that should you decide to join us as a client today, you have absolutely everything you need to get your very own portfolio from Motley Fool Wealth Management up and running with a minimum amount of time and effort required on your part, we are only opening the doors of Motley Fool Wealth Management to 1,000 new Fools at this time.

That said, my team and I are so proud of what we’ve created here in Fool Wealth, and we’d be delighted for you to be a part of it. So I hope to hear from you soon!

In the meantime, please enjoy Morgan’s article below, and Fool on.

Nick Crow, CFA

President

Motley Fool Wealth Management

6 Devastating Portfolio Mistakes You're Likely Making Right This Minute

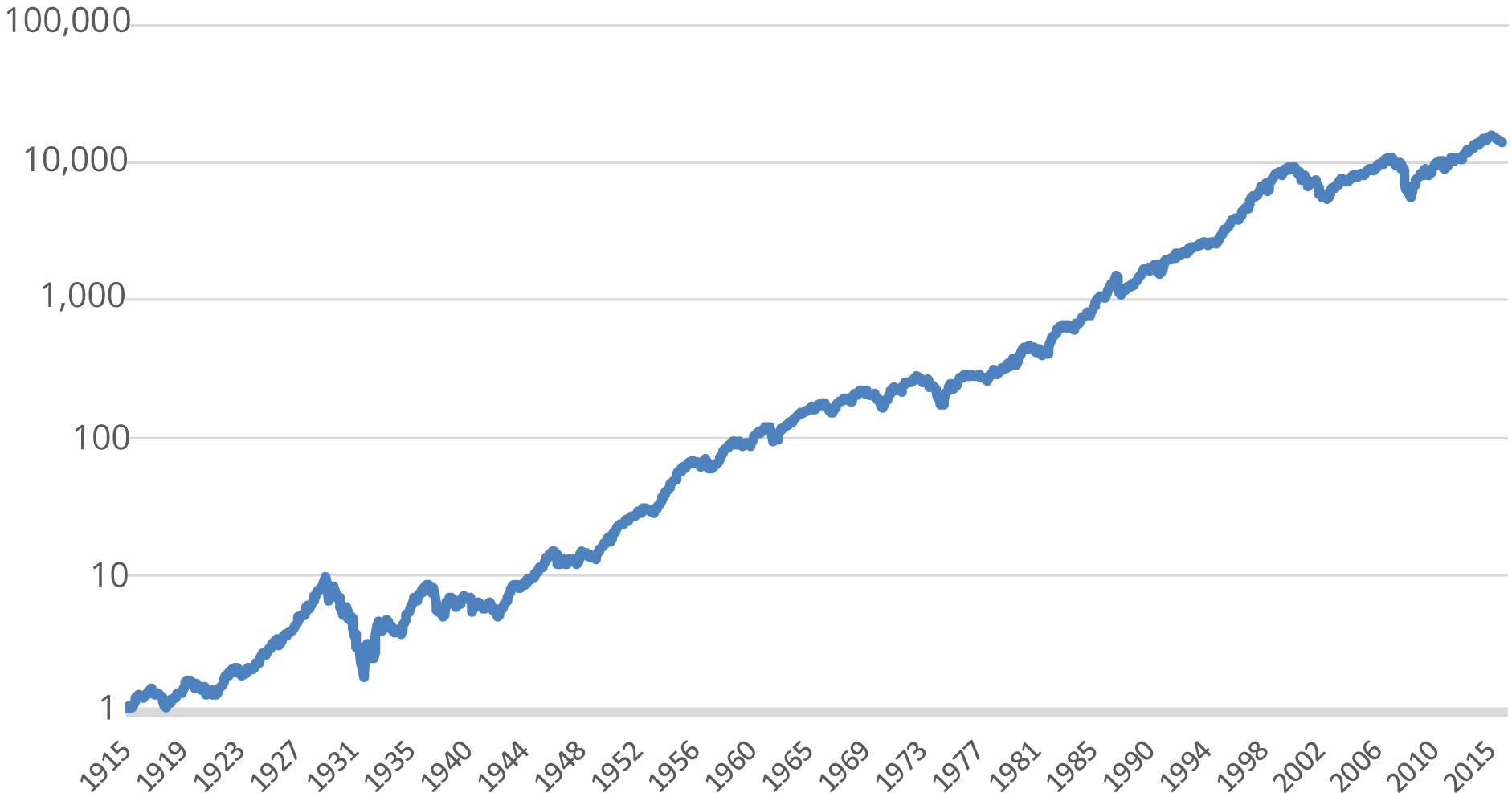

Take a look at this chart. It shows how much the S&P 500 grew over the past century:

One dollar invested in 1915 turned into $14,300 by December 2015. That’s the equivalent of turning a cheeseburger into a BMW.

Even if you account for inflation, the S&P 500 rose more than 2,000-fold over the past century.

During that time we had two world wars, four smaller wars, a flu pandemic, 18 recessions, several bouts of high inflation, terrorist attacks, floods, hurricanes, and earthquakes. Through it all, stocks still rose 2,000-fold.

The stock market has been the largest wealth-creating machine in the history of America. And just about any American with even a small amount of savings has been able to take advantage of it.

And yet, here’s the thing…

The stock market doesn’t have the greatest reputation among everyday Americans. People use all kinds of unsavory words and phrases to describe it …

“Crapshoot.” “Casino.” “Rigged.” “My 401(k) turned into a 201(k).” “Too dangerous.” I hear it all the time.

That’s why the single most important investing question we can ask is this:

“Why is there such a disconnect between how well the stock market has done over the past century… and how skeptical many Americans are of the market?”

After thinking about this question for most of the past decade, I’ve found six common investing mistakes people make that explain this disconnect.

#1: Not Realizing There’s A Price To Pay For High Returns.

There’s no such thing as a free lunch, the saying goes. If you want something nice, you must be willing to pay a cost.

The stock market has historically offered stellar long-term returns. Far better than cash or bonds.

Why? Not because someone’s being nice to you.

There’s a cost — a price of admission that must be paid.

The price of admission to earn high long-term returns in stocks is quite simple. Volatility.

You don’t actually pay this bill; it’s a mental surcharge. But it is very real. Not everyone is willing to pay it, which is precisely why there’s such a ripe opportunity for those who are.

If you look back at the history of the stock market over the past 100 years, you will see that volatility — even really heavy volatility — is strangely common. I counted every historical bout of market turbulence since 1915, which shows just how common losing a big chunk of your money can be:

- 90 times stocks fell at least 10% — once every 11 months, on average.

- 21 times stocks fell at least 20% — once every four years, on average.

- 9 times stocks fell at least 30% — once every decade, on average.

- 3 times stocks fell at least 50% — a handful of times in your lifetime, if you’re lucky.

Again, this was during a period when your money grew 2,000-fold, even adjusted for inflation. Yet you lost a fifth of your money an average of every four years.

If you don’t realize how perfectly common volatility is, you react to it differently. Maybe you think it’s a sign that the market is broken, so you sell. Perhaps you see it as a sign of permanent ruin, so you swear off stocks for good.

Never has this been true. Never. Volatility is simply the normal path any investor looking for long-term returns must be willing to deal with.

The greatest cause of the disconnect between the long-term returns of stocks and the skepticism many people have about the market is not understanding that volatility does not preclude long-term growth.

Indeed, volatility is why we have long-term growth. If stocks weren’t volatile, they wouldn’t be risky. If they weren’t risky, they wouldn’t offer greater opportunity than, say, a savings account. Why should they?

If you’re willing to pay the cost of volatility, the long-term gains can be great. But you must be willing to pay that cost. Remember, no free lunches.

#2: Assuming You Know When The Next Market Crash Will Come.

Now, we know how common volatility is and how often the market crashes.

But even if you’re familiar with how frequently stocks tumble, do you think you’ll be able to forecast the next decline? Or sell now and get out before things get ugly?

Let me tell you now: You can’t.

There have been four distinct turning points in the stock market when, in hindsight, stocks were peaking and about to quickly plunge.

One was in October 1929, before the Great Depression. Stocks crashed more than 20% in one day and went on to fall nearly 90%.

Another was in October 1987, before a one-day crash that took stocks down 22%.

A third was in March 2000, the peak of the dot-com bubble, before stocks lost more than a third of their value.

The last was in October 2007, before the recent financial crisis that made stocks lose half their total value.

I recently visited the Library of Congress in Washington, D.C., to read old newspapers from the days before these turning points to see if there was any clear warning.

Was anyone ringing a bell signaling a top? Even with the absurd benefit of hindsight, could I go back and spot the obvious market peaks?

Nope, not even close…

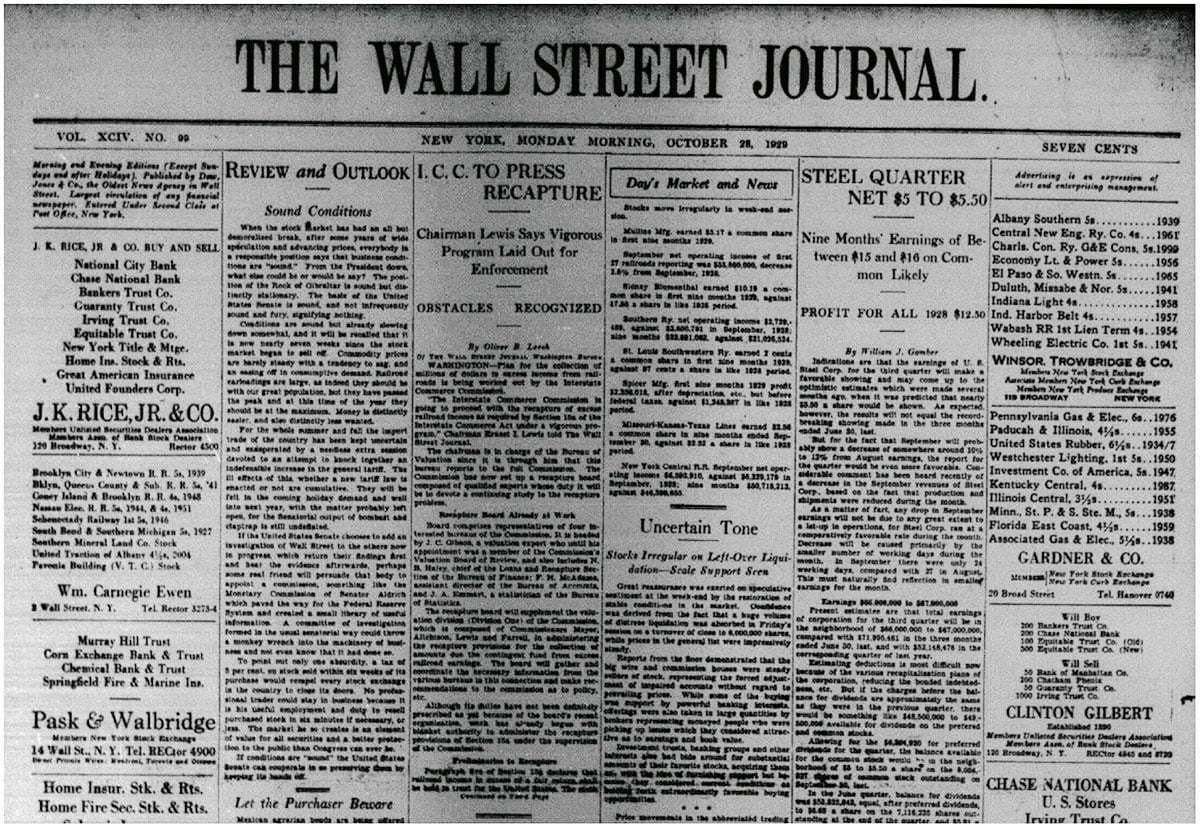

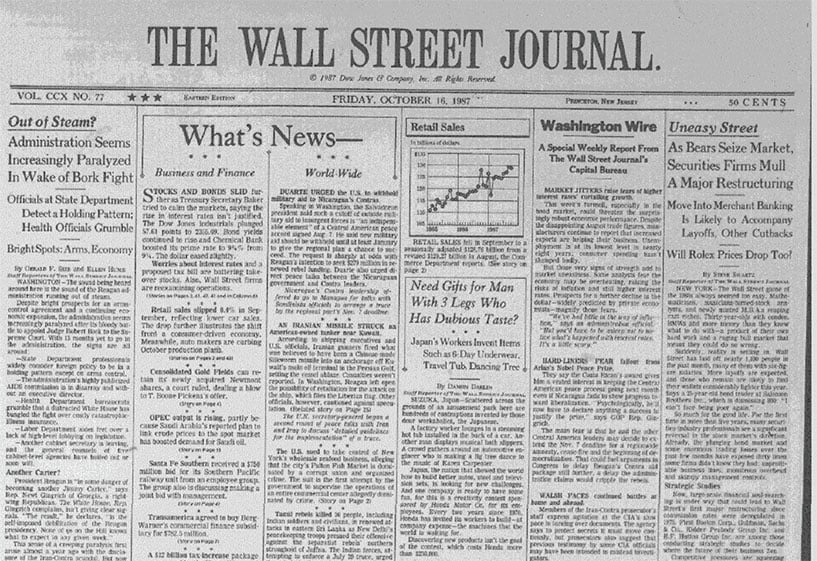

Here’s the front page of The Wall Street Journal on October 28, 1929 — the day before the start of the Great Depression.

You’ll see the top story of the day, under Review and Outlook, is titled “Sound Conditions.”

Another story lists a strong quarter of profits for U.S. Steel. Boring news.

Flip the page and you’ll find stories about Texas cotton exports, Treasury bill auctions, upcoming theater shows and reviews, the prospect of steel companies (“strong”), haberdasher sales (“custom shirts for $3”), and Dutch rubber production (“growing”).

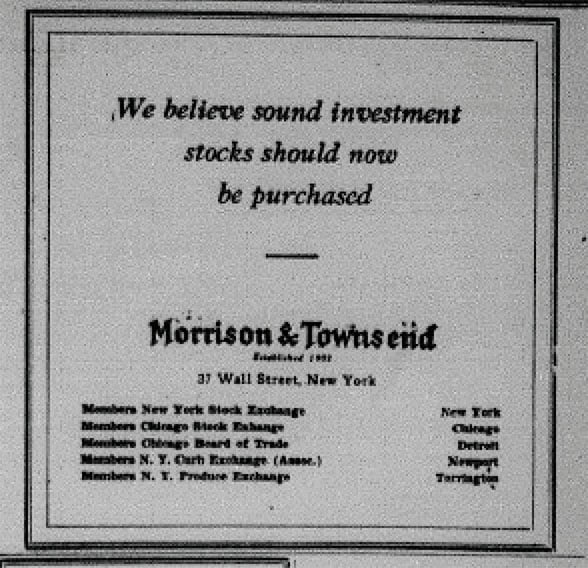

Nowhere — not a single place — does anyone announce that starting tomorrow, the world economy will collapse and push stocks down almost 90%. Instead, you’ll find this ad (I have no idea what happened to poor Morrison & Townsend):

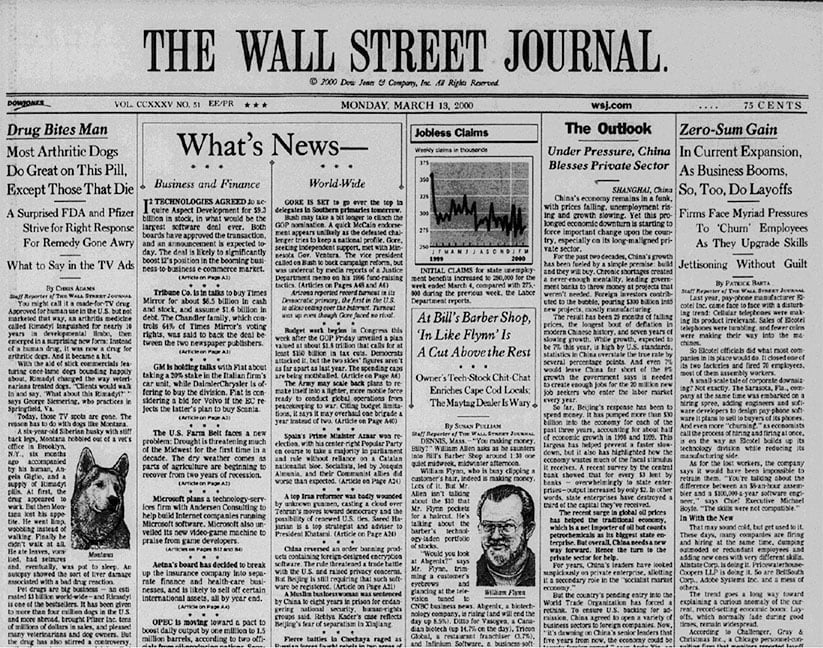

Here’s the WSJ on the day before the crash of 1987. Remember, this is the day before stocks lost nearly a quarter of their value. The top story was: “Need Gifts for Man With 3 Legs Who Has Dubious Taste?”

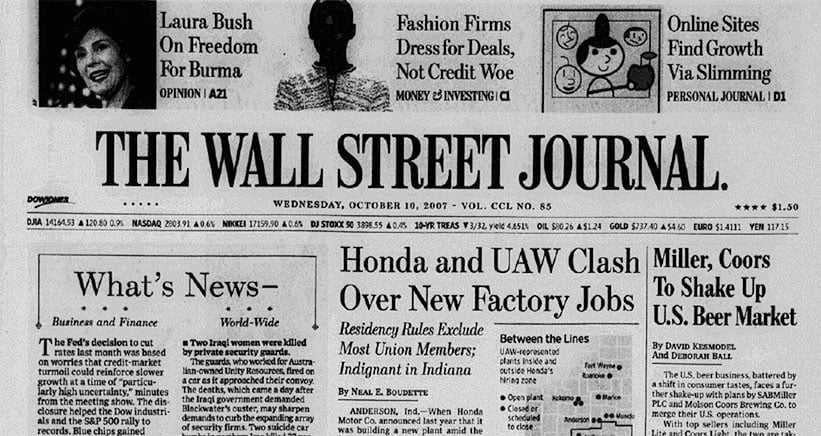

Here’s March 2000, on the day the great 1990s stock boom peaked. The top story is about Bill’s Barber Shop:

And here’s October 2007, when stocks peaked just before the recent financial crisis. The biggest news was Honda’s arguing with labor unions:

If I couldn’t spot an obvious market top with the benefit of hindsight while sitting in the Library of Congress, how do you think you’ll be able to spot the next market top using foresight alone?

You won’t. Which is why so few investors have been able to call market tops.

Predicting market crashes is sort of like predicting earthquakes in San Francisco. We know with pretty good certainty that San Francisco will have more earthquakes. We know with pretty good certainty that some of them will be strong. But no one can say there will be an earthquake tomorrow. Or next week, next month, or next year. They just don’t work that way.

Market crashes and earthquakes are as inevitable as they are unpredictable. I cannot stress this point enough, and here’s why. Because if you don’t realize this, you may be tempted to forecast the next decline and sell way too early… when in fact stocks may keep marching high for years to come.

Taking the long road and enduring, rather than avoiding, crashes is by far the most rational way to invest.

#3: Selling Your Winners Too Early.

There aren’t any certainties in investing. The smartest investors think in probabilities. The way you win at investing isn’t by perfectly predicting the future. It’s by setting up a portfolio that puts the odds of success in your favor.

Here’s the truth: Even the best investors get 40% to 70% of their stock picks wrong. But they can still outperform the market — even by a lot — as long as the rest of their portfolio does extraordinarily well.

Here’s an example. The Russell 3000, an index of America’s largest companies, increased 13-fold from 1987 to 2014. But during that period, 40% of companies in the index actually lost money. The overall index did well because 7% of companies increased tenfold or more, easily making up for the 40% of losers.

This is common whether you’re investing in an index or a portfolio of stocks. In a properly diversified long-term portfolio, the median holding will almost never perform well. The majority of the returns will come from a small minority of positions.

At last year’s Berkshire Hathaway shareholder meeting, Warren Buffett noted that of the roughly 500 companies he has invested in during his lifetime, he has made most of his money on 10 of them. His partner, Charlie Munger, mentioned the same, noting that if you remove just a few of Berkshire’s top investments, its long-term track record drops to average.

Investing is a game of probabilities. What matters is the performance of the portfolio as a whole, where a minority of winners make up for a larger portion of losers. “It’s not whether you’re right or wrong that’s important,” George Soros once said, “but how much money you make when you’re right and how much you lose when you’re wrong.”

When investors own a stock that does really well, there’s often an urge to sell. This seems like a prudent thing to do, because a growing stock makes up more and more of your portfolio. But the evidence is overwhelming: Over the long run, a small minority of your stocks will make up the majority of returns.

If you insist on selling winners too soon in an attempt to balance out your portfolio, the odds that you will even match the market index over the long run are slim.

#4: Taking Too Little Risk When You’re Young And Making Up For It By Taking On Too Much Risk When You’re Old.

I’ve given several presentations outlining the history of the stock market and the importance of investing for the long run. Five to 10 years, at least.

Every time I’ve said this, someone raises a hand and says, “Well, that’s great. But I don’t have five or 10 years. I need my money now, today, to live on. But I also need to earn a high return to fund my retirement.”

And several times I’ve given the same talk, a young person emails me and says, “Well, that’s great. Time’s on my side. But I don’t have any money to invest right now.” Of course you don’t. At this stage of your financial life all you care about is how to manage your student loans, which is literally the opposite of compounding interest.

A painful irony in investing is that the stock market works best for people who have decades to invest. But those people tend to have little money. By the time investors have a high income and can save a lot of money, they’re near retirement and don’t have time on their side.

This turns into a double whammy. People end up without enough to retire on, and then take too much risk while they’re in retirement to make up for it. When people need stock returns but can’t afford short-term volatility, they are bound to be disappointed.

This leads to frustration and gives investors a feeling that the stock market is a casino that cheated them out of their hard-earned retirement money. In reality, it didn’t. It’s just not meant for people who don’t have years in front of them.

Stocks just hit an all-time high. Nobody — not a single person — who has stuck it out in a diversified portfolio of U.S. stocks has ever lost money. But millions of investors have indeed lost money in stocks because they didn’t have the patience to stick it out.

There is a solution: It’s adjusting expectations and structuring a portfolio that meets your specific life goals. Creating a realistic mix of stocks, bonds, and cash that lets you sleep at night is absolutely critical to getting the most out of the stock market.

#5 Having An Extreme Bias Toward Action.

In most fields, the harder you try, the better you do. Tiger Woods used to hit thousands of balls at the range. Musicians practice daily for their entire lives. Doctors, mathematicians, lawyers, and engineers are constantly working, fiddling, tweaking, and changing their procedures to find better ways to work.

Investing is different. The evidence, from academic studies and anecdotes of professional investors, is overwhelming: The more you fiddle with the knobs — trading in and out, selling this, buying that, flipping this, being concerned about that — the worse you’ll do over time.

Trading generates fees. It triggers tax bills. And most important, it’s predicated on the idea that you know what the stock market will do next, which history shows nobody does.

Part of the problem is the financial industry itself.

Financial advisors come in two groups. There are stockbrokers, who don’t have a legal obligation to put your best interests first. They often generate their income based on commission. Of course, the more actions they can take in your portfolio, the more commissions they generate for themselves. There are also Registered Investment Advisors, who have a legal fiduciary duty to put your best interests first.

The only consistent way people can make money in stocks is to let company profits and dividends accrue over time. When you own shares in a company, that company will hopefully make some profit today. And a little more tomorrow, next week, next month, and next year, growing those profits along the way. As an owner of those companies, you accrue profits over time. That’s ultimately what drives the stock market higher over time.

Reaping these gains doesn’t require day-to-day action. It requires a lot of waiting and patience, but not much else.

One of the biggest challenges investors face is not realizing that once you have a portfolio of high-quality businesses, investing is largely a hands-off endeavor. You just sit back and let company profits accrue. But since this runs counter to how you get better in most other fields, it’s incredibly hard to come to terms with. Which is why so many investors fail at it.

“The big money is not in the buying or the selling, but in the sitting,” investor Jesse Livermore once said.

#6 Not Knowing Your Own Behaviors And Biases.

One of the most important lessons I’ve learned about investment biases is that people are terrible at predicting their future emotions.

Every investor I know says they’ll be greedy when others are fearful. They never assume that they themselves will be the fearful ones. But someone has to be, by definition.

No investor wants to think they’ll panic and sell if stocks fall 20%. They’re more likely to say that a 20% decline would be a buying opportunity. This is the right attitude, but the reason there will be a 20% crash is specifically because some investors choose panic selling over opportunistic buying.

My experience is that most investors who say they’ll be greedy when others are fearful soon realize that they are the “others.” It has to be this way: When everyone thinks they’re a contrarian, at least half will be wrong.

When investors are bad at predicting their emotions, sticking to their financial goals becomes difficult. I can say I plan on investing $500 a month each month for the next 30 years. Or I can assume that I won’t sell when the next market crash comes. But those goals rely on the assumption that I can behave the way I’d like to in the future. And that’s an altogether dicey assumption to make.

I have found that the best way to get a realistic picture of my future emotions is to document my past emotions. You can do this by keeping an investing journal.

Every investor, no matter how active or passive, should have an investing journal. It doesn’t have to be elaborate. Just document how you’re feeling when you make investment decisions.

If you keep a detailed journal of your feelings and emotions when making investment decisions and review it over time, I think you will notice that how you expected to feel when the market falls, or surges, is far different than how you actually feel. Coming to terms with these feelings and being realistic about what kind of investor you are are absolutely critical to setting yourself up for long-term investing success.

If your history shows you have a low risk tolerance, that’s fine! Be realistic and set up a portfolio that acknowledges that personality.

Take a look again at the chart at the top of this report. The market has historically been an extraordinary generator of long-term wealth. It will almost assuredly continue to be in the future. The great news is that by understanding and avoiding the simple flaws most investors suffer from that prevent them from capturing that wealth, a piece of that pie can be yours.

To discover what we can do for you, simply click the button below to speak with a wealth advisor.

Already a client? Simply click the button below to see your accounts.