Have you thought about buying an annuity for your retirement income?

You’re not alone. Many individuals consider annuities to provide a steady stream of income in retirement. And even if you hadn’t thought about buying one, your financial advisor may have steered you in that direction at some point. Why? One reason is that some annuities have features that sound incredibly appealing to many people, even if they are suitable for only a certain segment of investors. For example, “guaranteed cash flow ‘til you die.” Who doesn’t like the sound of that? So, an advisor may feel obliged to discuss them with you.

The other is that annuities are very profitable for advisors. So, no matter how good your advisor is about not selling you products you don’t need, he/she may not be able to resist presenting annuities to you, in case you love the presentation and want one.

Unfortunately, many annuity buyers decide, a few years after buying one, that they don’t want it—sometimes because they realize they can make better returns elsewhere and other times because they must cancel the annuity if they want access to the principal.

One study reports an astonishing 95% of annuities are never annuitized (held to when the income stream starts) by the investor.1 They are cashed in, despite cancellation penalties, before they deliver their lifelong cash flows. This wastes investors’ money, and suggests the annuities were either not properly explained in the first place or are simply inappropriate for many buyers.

To avoid making this mistake, we’re going to do what is rarely done: Explain in simple terms the pros and cons of annuities, and who they are best suited for—so you can decide if one is right for you…before you buy.

What are annuities, and why are they appealing?

Annuities are insurance products that pay out steady income in exchange for a nonrefundable upfront investment. There are many kinds, depending on the type of income payout you want: fixed income, variable income, indexed income (payout linked to an index such as the S&P 500), immediate payout, delayed payout and more.

Their strongest appeal is that the income is guaranteed. Let’s be honest. Income created by stock and bond investments can fluctuate—sometimes by a lot—during market pullbacks or company failures. Income from annuities is guaranteed by the insurance company. The insurance company bears all the risk, not you.

Sounds great, right?

The problem is, you must pay the insurance company for bearing all the risk to guarantee your steady income, no matter what the market does—possibly for a lifetime! This can be expensive.

To make the money they guarantee to pay you, insurance companies must invest your principal in very low-risk investments, which invariably can generate low returns. Then to ensure they can pay you even if the markets go down, they must keep a lot of the return in order to build up a significant buffer (this is the insurance business, after all). Then of course, being a functioning company, they must pay their employees and their shareholders. To afford this, they may charge additional fees. In other words, to get a guaranteed income from your annuity, you must pay for a skilled insurance middleman, who often keeps a portion of your return (typically to pay sales commissions but also possibly to insure against potential payouts that are higher than market-generated returns). This may seem to be very inefficient for you.

Is there a better way to get a secure income?

There are two ways to invest for financial security over a long retirement.

One way to get long-term financial security is to eliminate risk altogether, which is what annuities try to do.

The other way is to minimize risk by minimizing fees and maximizing growth and income, using a well-crafted portfolio of stocks and bonds. This strategy may generate a much higher return for your money. But how can you minimize the risk that an inevitable market correction will choke off your income? That requires financial planning and a steady temperament.

A professional financial planner uses tools to model your portfolio and test it against various possible future market outcomes. This helps you to choose strategies that take into account your spending needs and wealth goals to strive to maximize your chance for living the retirement you want.

Let’s walk through a hypothetical example.

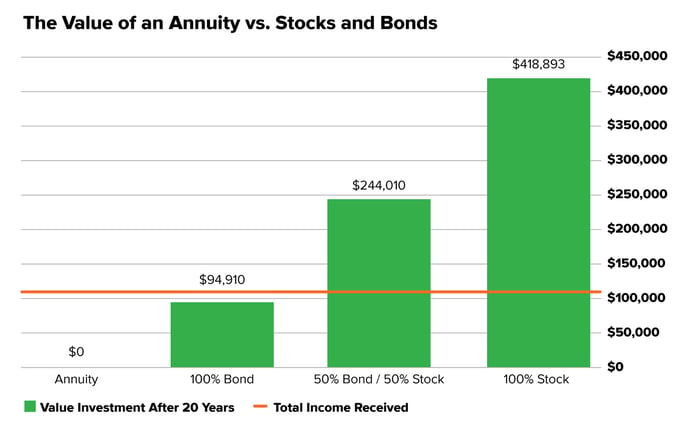

Dan just turned 65 years old and is concerned about having enough income to supplement his Social Security payments. Dan has $100K available that he can hold in cash, buy an annuity, or invest in marketable securities. His friend talked to him about the immediate annuity he just purchased. Dan is unsure if he should buy one too, so he reached out to his financial planner.

After explaining the advantages and drawbacks, his planner compared the returns of a typical annuity to average returns of stock and bond portfolios. She estimated Dan’s life span to be about 85 years old—another 20 years from today—since Dan’s relatives lived to 83 years old, on average. They also reviewed Dan’s spending needs and determined he’ll need about $455 each month to supplement his Social Security income.

Here are the results of the analysis:

The annuity calculator determines income based on a group of reputable insurance companies available through The Fidelity Insurance Network. See methodology and assumptions. The bond and stock portfolios were calculated by Bankrate.com. To calculate the U.S.market returns, Vanguard used the Standard & Poor’s 90 Index from 1926 through March 3, 1957; the S&P 500 Index from March 4, 1957, through 1974; the Dow Jones Wilshire 5000 Index from 1975 through April 22, 2005; the MSCI US Broad Market Index from April 23, 2005, through June 2, 2013; and the CRSP US Total Market Index thereafter. For U.S. bond market returns, Vanguard used the S&P High-Grade Corporate Index from 1926 through 1968, the Citigroup High-Grade Index from 1969 through 1972, the Lehman Brothers U.S. Long Credit AA Index from 1973 through 1975, the Bloomberg Barclays U.S. Aggregate Bond Index from 1976 through 2009, and the Bloomberg Barclays U.S. Aggregate Float Adjusted Index thereafter. The rate of return was based on the historical average return from 1926 to 2019: 100% bond is 5.33%, 100% stock is 10.29%, and 50%bond/50%stock is 8.29%. Sources: Vanguard, Bankrate.com, Fidelity.com

As you can see, Dan would be significantly better off if he does not buy an annuity, and instead invests in any of these portfolios, with the best being the 100% stock fund. But what if he lives another 30 years instead?

The results do not change. The total income after 30 years is speculated to potentially be $163,800 ($455 per month for 30 years) from each. But the bond and stock portfolios would continue compounding and have significant value left at the end of the 30-year period.

So how could Dan structure a portfolio to provide the monthly cash he needs?

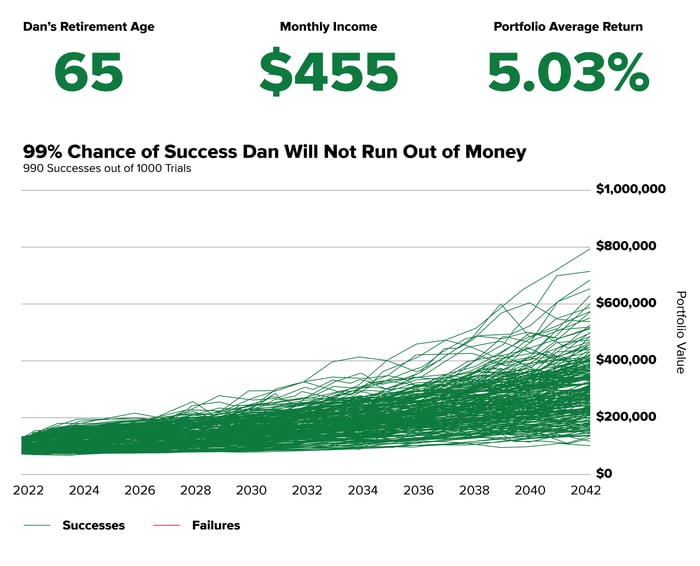

Dan’s advisor recommended a two-pronged approach.

First, she suggests a cash carve-out strategy. This solution sets aside three years’ worth of living expenses in a mixture of cash and fixed income (including money market funds). It’s like your living expenses paycheck. For Dan, that would be $16,380.

Second, with the remainder—$83,620—she recommends a portfolio that consists of bonds with various maturities, which would “ladder” their payments and a combination of dividend-paying and growth stocks. That way he potentially could receive a more structured, although not fully guaranteed, income stream while continuing to grow his portfolio.

Since Dan is concerned about inflation and a market decline, his advisor suggested he take on less risk. She proposed a more conservative portfolio that has returned 5.03%, on average per year. Her analysis also accounts for inflation at 2.25% per year. Here is the modeled outcome of the suggested plan:

Source: MoneyGuidePro. The return assumptions in MoneyGuidePro are not reflective of any specific product, and do not include any fees or expenses that may be incurred by investing in specific products. The actual returns of a specific product may be more or less than the returns used in MoneyGuidePro. It is not possible to directly invest in an index. Financial forecasts, rates of return, risk, inflation, and other assumptions may be used as the basis for illustrations. They should not be considered a guarantee of future performance or a guarantee of achieving overall financial objectives. Past performance is not a guarantee or a predictor of future results of either the indices or any particular investment. IMPORTANT: The projections or other information generated by MoneyGuidePro regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. MoneyGuidePro results may vary with each use and over time. Other disclosures and a glossary are available at moneyguidepro.com.

Of course, no one can predict future returns, so Dan must be comfortable taking on the risk of a market decline and committing to remain invested even through those inevitable market downturns. However, the above return calculations are based on over 90 years of data, which should provide some comfort.2

Another notable difference? Dan would pay the ordinary income tax rate on the income he receives from his annuity. Conversely, he would pay the long-term capital gains rate on the income from the portfolios assuming the investments are held for more than one year before selling. Today the median tax rate is 24% while the highest bracket is 37%.3 Contrastingly, the 2022 long-term capital gains rate is 15% for most investors, while the highest income earners will pay 20%.4 That could be a significant difference depending on his tax status in retirement.

Are annuities right for you?

Annuities are a good option for some investors. For example, individuals who cannot stick to their wealth plan in the event of a market downturn—whether they’re unable to stomach losses or can't afford to lose capital—may be candidates for an annuity. But if you are a person who can follow a financial plan, live within a budget, and manage your emotions during market dips, then generating income from stocks and bonds—as Dan did—could be a better approach. Why pay the middleman when you can potentially reap all the rewards!

Related Articles

3 Wealth Planning Strategies at Every Life Stage

Wouldn’t it be nice if retirement happened without fuss or bother? Better yet, if you had an...

Retirement Planning for Spouses with an Age Difference

Retirement planning for a married couple can be complex, especially if there is an age difference...

Annuities Explained

Do you ever think about what it would feel like to win the lottery? (Actually, one or two of you...