Do you feel you pay too much tax each year? It's (probably) a rhetorical question! We believe most working people think Uncle Sam takes too much of their hard-earned cash. Many retirees probably feel the same way—especially because their income comes primarily from the fruits of their younger selves' labor. But unlike working individuals in the accumulation phase of their lives, retirees' income is generally fixed. As a result, any tax increase may harm their living standards. So as a retiree (or anybody, really), you may be wondering if there is anything you can do to lessen the blow.

While we don't subscribe to skipping out on your debts and obligations, some strategies (legal maneuvers, in case you're wondering) can help lower your tax bill in retirement. Here are three options to consider.

Retirement income

Retirement income often comes from several sources. Many retirees receive Social Security and some form of an employer-sponsored retirement plan—like a pension or 401(k)—or have an IRA. And to supplement that income, some also have a taxable investment account, like a brokerage account.

Individuals who receive Social Security benefits or take distributions from an employer-sponsored retirement plan or traditional IRA generally pay ordinary income tax rates on that income stream. However, income that comes from a taxable investment account that is held for over a year is taxed at long-term capital gains rates.

Income tax rates are generally higher than long-term capital gains rates for many people. With that said, most people want to avoid paying upwards of 37% on their investment gains. Here are three strategies to potentially mitigate tax on investment gains.

3 tax-mitigating strategies

Before we go into these strategies, we have two warnings. First, implementing some of these strategies takes work. Second, every individual's circumstance differs. Motley Fool Wealth Management does not (and is not permitted to) provide tax and you should consult a tax professional when making any tax decisions.

Strategy 1: Avoid short-term capital gains

This first strategy is perhaps the simplest to implement, but, at times could be emotionally challenging. Why an emotional decision? Because investors often make up their minds to sell and want to do it right away. But long-term capital gains are preferable to short-term ones, AND you need to hold your investments for more than one year to avoid short-term capital gains.

Tax rates for long-term capital gains are up to 20%, whereas short-term capital gains rates fall between 10%-37%, the same rate as ordinary income. For example, if you and your spouse have $500K in capital gains, you much prefer to be taxed 15% than 35%!

Let’s walk through a hypothetical example to put this in perspective.

Joe and June are considering selling two stocks. They've held Stock A for 11 months and Stock B for 13 months. They’ll recognize a $100K capital gain on each of them. How does their after-tax profit differ?

| Stock A | Stock B | |

|---|---|---|

| Holding Period | 11 months | 13 months |

| Initial Investment | $500,000 | $500,000 |

| Gain | $100,000 | $100,000 |

| Tax Bracket | 32% | 15% |

| Tax on Gain | $32,000 | $15,000 |

| After-tax profit | $68,000 | $85,000 |

| Annualized pre-tax return | 21.9% | 18.4% |

| Annualized after-tax return | 14.9% | 15.6% |

Difference in after-tax profit: $17,000

Source: Motley Fool Wealth Management. For illustrative purposes. The illustration is for a married couple filing jointly with an annual income of $400K. The analysis ignores the net investment income tax, which would add a 3.8% charge on investment income in both scenarios.

By waiting just two months, (assuming that the capital gain is equal for illustrative purposes), Joe and June keep an extra $17,000 of the investment profit. Said a different way, they would put 17% more of their profit in their pockets instead of paying it to the government!

Strategy 2: Match gains with losses

No one likes to sell their investments at a loss. But if you no longer believe in why you purchased the security, or want to hold fewer shares, then selling it at a loss can help offset gains from a tax perspective. This process is commonly known as tax-loss harvesting.

So not only do you remove a company from your portfolio that you no longer believe in, but you can also help offset taxes on the sale of an appreciated security. Here’s an illustration of how it can work:

Matthew and Kelly want to reduce their exposure to Z company but are worried about the tax consequence of realizing the stock’s appreciation. They recently sold Stock Y for a loss. Their advisor sent them the following analysis to show how they can sell some of their shares in Stock Z and not pay any capital gains taxes.

| Stock Y | Stock Z | |||

|---|---|---|---|---|

| Year | Action | Cost | Action | Cost |

| 2018 | Bought 100 shares for $200/share | $20,000 | Bought 100 shares for $50/share | $5,000 |

| 2021 | Sold 100 shares for $100/share | $100,000 | Sold 75 shares for $200/share | $15,000 |

| Total Gain (Loss) | ($10,000) | $10,000 | ||

% Gain Offset: 100% Total Taxes Paid $0

Source: Motley Fool Wealth Management. For illustrative purposes only.

Since they recognized a loss of $10,000 when they sold Stock Y, they can sell 75 shares of Stock Z at the market price of $200/share for a gain of $10,000. Because the capital gain equals the realized loss, they should pay zero taxes. Furthermore, Matthew and Kelly could use up to $3,000 of net losses against other income. This is a way to use capital losses more efficiently against ordinary income, such as wages, which, as we said, are typically taxed at a higher rate.

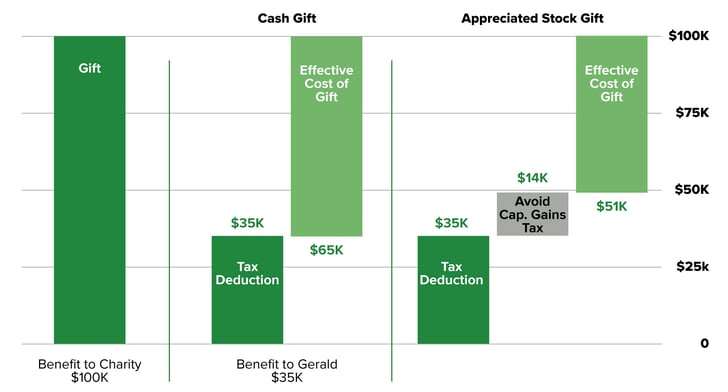

Strategy 3: Donating your appreciated stock

When you have a security that has appreciated considerably over a holding period of one year or more, you can donate that security to a charity and receive a charitable income tax deduction for the security’s fair market value. In other words, you can reduce your income and incur a lower tax bill as a result.1 In addition, when you donate an appreciated security, you can avoid the capital gains tax you otherwise would have to pay if, instead, you sold it.

So should you donate cash or an appreciated security?

Consider this example: Gerald would like to donate to a charity in his mom's name. While weighing the trade-off between giving cash or an appreciated security, here's the analysis his advisor showed him:

For illustrative purposes only. Gift to a qualified public charity. Federal tax rate: 35%. Long-term capital gains rate: 20%. Stock basis: 30%.

If Gerald makes a $100,000 cash donation, it could result in a charitable tax benefit of $35,000, effectively lowering the cost of the gift to $65,000. But by donating a security, Gerald can take the charitable tax deduction ($35,000) plus the benefit of not having to pay tax on the stock’s appreciation ($14,000), for a total effective gift cost of ($51,000). And if Gerald still wanted to hold that security in his portfolio—because he transferred and did not sell it—he can use the $100,000 of cash he has set aside for a cash donation and repurchase the security immediately, thus resetting his cost basis.

Think after-tax income

If you win a $1 million lottery, do you get the full million? Likely not. You'll probably get the lump sum portion minus taxes—possibly around the $300,00-$400,000 mark. Still a windfall, but certainly not a $1 million windfall!

Like with the lottery, all income should be framed in the after-tax sense. That may mean holding off on selling a security for a few weeks or longer, getting rid of losers, or giving away winners.

Strategizing on how best to recognize your investment gains could mean the difference of thousands of dollars or more in your bank.

The strategies discussed above and others are often complicated to implement. So, it's important to consult a tax professional and a Wealth Advisor to understand your plan from a holistic perspective and the potential general tax consequences of your moves.

Have a large position in one stock? Check out our blog on how to handle a large, concentrated stock position.

Related Articles

3 Ways to Lower Income Tax in Retirement

Even if you’re not working in retirement, you probably generate income and pay tax on it. How, you...

What Every Retiree Should Know About Taxes

Tax planning doesn’t end with retirement. In fact, tax planning can be equally, if not more...

A Backdoor Roth IRA: What's All the Hoopla?

"Backdoor" Roth conversions have been widely touted as a "rich person's Roth." That's because if...