Does a market dip make you cringe and hope that your money is safe? While there’s no fool-proof way to protect invested assets fully, there are ways that can help better insulate money against market drawdowns. Employing the “right” asset allocation is one of the most powerful ways. Here’s how it works.

Asset allocation models: The nuts and bolts

Asset allocation determines the percentage of each asset class in a portfolio. It allows investors to "balance out" the potential risks and returns to help them reach their wealth goals. This balancing act can be essential because a too risky portfolio may have the potential to deliver outsized returns but also make it vulnerable for massive drawdowns. On the other hand, a too conservative portfolio may leave money on the table.

Asset allocation often works because market conditions that create poor or average returns in one asset class may boost others. Therefore, a proper mix of asset classes may lower the volatility of investment returns without sacrificing potential gain.

An asset allocation model is the thinking and assessment behind building an asset allocation recommendation.

While this is important for all investors, it’s even more crucial in retirement when investors don't have the time horizon or earnings to offset significant portfolio losses.

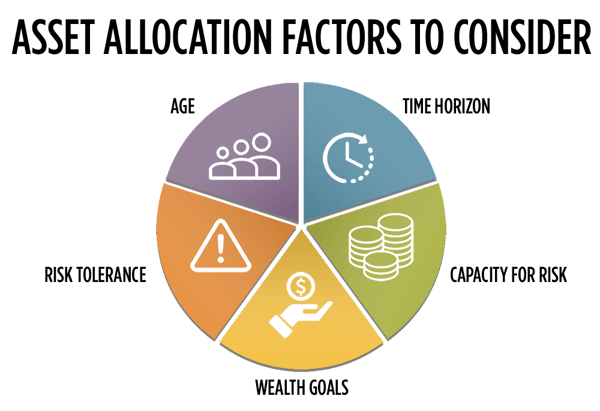

Is there such a thing as the “right” allocation for me?

Yes, there can be. Every person has a unique vision of life and how to live it—both of which influence spending and saving. That vision, in conjunction with certain factors, should drive their unique optimal asset mix.

How asset allocation models work

Most models analyze the above factors and provide guidelines and recommendations on how to split a portfolio among various investment types. In many models, that includes:

- Stocks

- Bonds

- Cash

- Other investments

Typical allocations recommend a combination of several asset types to diversify portfolio risk. However, they also need to focus on meeting short-term expenses while growing assets for the future. This dual objective—to meet short- and long-term wealth expectations—is why some allocation models may favor a higher weight in stocks than other asset classes.

One of the best paths to achieving long-term wealth can be primarily through stocks. That’s important for individuals at all life stages. Those in their earning years can be trying to accumulate and grow assets for their future. At the same time, retirees may need income to meet living expenses. But whether you’re a while from retirement, getting ready to take the plunge, or in retirement, don’t forget to account for inflation, which could eat away at a nest egg over the years.

The “typical” asset allocation process

Investors can arrive at asset allocation in a bunch of different ways. Some use age-based profiling, while others stick to the classic 60/40 approach. Many firms develop asset allocation models that fall into a few buckets from conservative to aggressive from these approaches. Investors are placed into the "best fit" model portfolios, but they are often not a perfect match with few options to choose from.

We think there’s a better way.

Asset allocation, the "Foolish" way

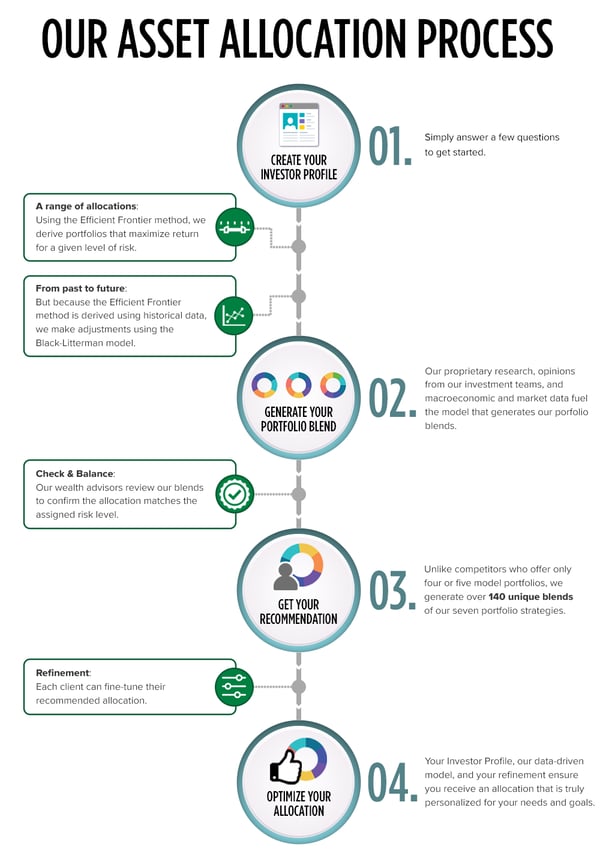

We don’t try to squeeze individuals into one of only a few broad groupings. We understand that individuals have distinct preferences and proclivities. So instead of three or four broad groupings, we offer over 160 different blends of seven investment strategies.* And because life is not static, the blend is also not set in stone. Asset allocations change as circumstances evolve. Here’s how our model works:

Our asset allocation model looks at risk and return preferences by individual needs and goals. To match the preferences with an appropriate allocation, our model considers many factors, including:

- the market risk-free rate

- the equity risk premium

- market capitalization of investments

- historical return and volatility of the equity markets

- unique insights from our portfolio management team and wealth planners on their relative views of the markets and economy and how they may differ from other investors

- proprietary trade data

The inputs to this model are updated regularly to reflect changes in our views, or market and economic shifts. We are constantly comparing our model’s recommendations to the sentiment of our team to ensure that it aligns with our planning advice. But just like any asset allocation tool or rule of thumb, this isn’t a substitute for human guidance. That’s why the refinement part of the process is so important.

The rebalancing act

One of the benefits of having a team of wealth planners and portfolio managers actively managing portfolios is the reassurance that an investment mix remains within the potentially optimal allocation.

At times, the performance of some portfolio holdings may push the portfolio mix outside its targeted range. For example, say your target calls for 60% of your assets in stocks. Then suppose your stocks have an outstanding year—and your exposure balloons to 75% of your portfolio. You might want to slide some or all of that extra 15% into other asset classes—thus "rebalancing" your portfolio.

Asset allocation models: Effective, not just convenient

Asset allocation models should serve one overriding purpose—to help investors determine their potentially optimal mix of securities for their unique needs.

But all too often, they’re used as a convenient way to herd investors into a broad grouping to ease the operational pressures of managing too many accounts. That makes sense up to a point—it would be quite challenging to manage an infinite number of accounts.

But using a few broad groupings fails investors who may have slightly different objectives. Instead, a model should be able to account for individual nuances and adapt based on them. In other words, a model needs to be effective, not just convenient.

Related Articles

Do You Have a Family Wealth Plan?

What does “real wealth” mean to you? Many people automatically answer with a dollar sum—a million...

New Job? Should You Roll Over Your 401(k)?

Transitioning to a new employer can be stressful. And for most people, their retirement account is...

Are the Latest Investment Trends Changing the Rules of Investing?

Meme stocks. Non-fungible tokens (NFTs). Robinhood. It seems that there's a new way to invest or an...