If you recently decided to start saving for retirement or you’re fine-tuning your approach, pat yourself on the back. You just made a lot of people happier—even if they don’t know it yet.

Having a smart retirement savings plan should make you more financially secure in the last third of your life and probably more independent, healthy, and happy. This can take a lot of work and worry off the backs of your spouse, kids, siblings, and friends.

401(k)s, traditional IRAs, and Roth IRAs are the most popular investment accounts in which to build retirement savings, and for good reason. Used properly, they can help you build a large retirement chest over your career.

All three accounts offer tax savings versus investing in a regular brokerage account. They also all provide an incentive to keep the money in the account until you retire (otherwise, you’ll pay a penalty for early withdrawal). And al three can make it easier to save for retirement, to varying degrees.

But in other ways, they are different. And knowing these differences can significantly affect how much you save.

How a 401(k) works

401(k)s are retirement investment accounts offered by companies to help their employees save for retirement. If you sign up for your company’s 401(k) program, it will take automatic pre-tax deductions from your paycheck (you choose the amount), put the money into your personal 401(k) account, and invest the money according to your investment selections. Most offer a variety of investment options, from conservative to aggressive, to fit your comfort. The service may also come with investment advice.

Companies may also offer you “matching contributions” up to a certain amount, such as 2%-4% of your salary. This benefit is like “free money.” For someone making $75,000, a 4% annual contribution is $3,000 of free money per year. Over 30 years, that is $90,000 in free contributions. These company contributions could grow significantly depending on how you invest over several decades.

For example, if the $3,000 was invested each year in a moderately conservative portfolio consisting equally of stocks and bonds that produced an average annual return of 6%, then after 30 years, that free money could be worth $237,174. Not a bad haul!

And this doesn’t even include your contributions. Since these are matching contributions, adding both together could produce a substantial nest egg.

But there is an important tax distinction to take consider: The money taken from your paycheck and added to your 401(k) is not tax-free. Rather, it is tax-deferred. You pay no income tax on it until you withdraw it from your 401(k), which should not be until retirement. The advantage of tax deferral is that most people are in a lower income tax bracket in retirement than in their earning years. By deferring tax payments until retirement, you can possibly pay a lower tax rate on your accrued savings.

How important are these tax savings? Let’s say your total retirement contributions over your career are $500,000. While working, your average tax rate is 25%. In retirement, your income could be much lower, so your average tax rate, for example, could be 15%.

If you don’t put this money in a tax-deferred vehicle like a 401(k), you will pay $125,000 in taxes as you earn it before retirement.

If instead you do use a tax-deferred 401(k) and delay paying income tax on it until you withdraw the money in retirement, you will pay only $75,000 in taxes on these contributions, for a potential savings of $50,000.

How much can you contribute to a 401(k) in 2023? Under the age of 50, you can contribute up to $22,500 per year into a 401(k). Those older than 50 can contribute an additional $7,500 per year ($30,000 total). But when you contribute this money, it’s essentially out of your reach until age 59½, or you’ll incur an early withdrawal penalty. This punishment usually squashes the temptation to take the money out early.

One potential drawback with a 401(k) is the required minimum distributions (RMDs) that participants must take each year starting at age 73. There’s only one way around this: If you are still working, then you may not have to take RMDs (unless you own more than 5% of the company). So even if you don’t need the money to supplement your retirement income, you must take it (or lose it) and pay taxes on the withdrawals.

How a traditional IRA works

IRA stands for Individual Retirement Account. They are generally opened and operated by individuals, not companies. There are two common types of IRAs: traditional IRAs and Roth IRAs.

Traditional IRAs are similar to 401(k)s in that the money invested is tax-deferred until it is withdrawn in retirement. How much can you contribute to a traditional IRA in 2022? Up to $6,500 per year if under age 50, and up to $7,500 if over 50—much less than a 401(k).

It works like this: After opening an IRA brokerage account, you transfer money from your personal accounts into the IRA. This money has already been taxed. So how do you get the tax deferral? You must claim and deduct the contribution on your tax return. Then years later, when you withdraw the money during retirement (after age 59½), you pay the income tax.

And like with 401(k)s, traditional IRAs force you to take required minimum distributions each year. However, unlike the “working exemption” with the 401(k), there’s no way around taking RMDs with a traditional IRA.* Again, you must take it (or lose it) every year starting at age 73 and pay taxes on the withdrawals.

Understanding Roth IRAs

Roth IRAs are similar to traditional IRAs in the amount of allowable annual contributions and how they are opened and operated. But the big difference is with tax treatment: Roths are not tax-deferred. Instead, you contribute after-tax money (so you cannot take a deduction on your tax return for your contribution). But they offer tax-free growth. When you withdraw your money in retirement, you pay no tax at all.

One difference with Roth IRAs is you can withdraw your contributions after 5 years with no penalty. However, the growth from these contributions—what you earned on the money you contributed—will incur a 10% penalty if withdrawn before 59½.

Another difference? Required minimum distributions during your lifetime are not mandatory. So, if you don’t need to withdraw funds throughout retirement, you can potentially leave your beneficiaries a sizable, tax-free inheritance.

But not everyone is eligible to make contributions to a Roth IRA. To qualify, an individual’s modified adjusted gross income (MAGI) must be below certain thresholds. (Consult with a professional advisor to determine your eligibility.)

Comparing 401(k)s, traditional IRAs, and Roth IRAs

| 401(k) | Traditional IRA | Roth IRA | |

|---|---|---|---|

| Administered by | Third-party administrator chosen by the employer | Individual | Individual* |

| Contribution Frequency | Deducted from payroll and benefits from dollar-cost averaging | At least annually before tax-filing day for prior tax year | At least annually before tax-filing day for prior tax year |

| Money Contributed | Before-tax | After-tax but eligible for a tax deduction | After-tax |

| What is it taxed? | At withdrawal | At withdrawal | Potentially never. Grows tax-free |

| Annual contribution limits before age 50 (after age 50) | $22.5K ($30K) | $6.5K ($7.5K) | $6.5K ($7.5K) |

| Maximum income limit | None+ | No limit, but the ability to take a tax deduction varies depending on filing status (married vs. single) and if you or your spouse has a retirement account at work# | $228K (married) $153K (single) |

| Penalty for withdrawal before age 59½ | 10% | 10% | No penalty on contributions. 10% on earnings only unless meet 5-year rule |

| Penalty exceptions | If the participant has a total and permanent disability; for unreimbursed medical expenses, depending on the amount relative to your adjusted gross income. | If the owner has a total and permanent disability; for qualified first-time homebuyers up to $10K; for health insurance premiums paid while unemployed; for unreimbursed medical expenses, depending on the amount relative to your adjusted gross income. | If the owner has a total and permanent disability; for qualified first-time homebuyers up to $10K; for health insurance premiums paid while unemployed; for unreimbursed medical expenses, depending on the amount relative to your adjusted gross income. |

| Investment options | Often limited | Unlimited | Unlimited |

| Required minimum distributions? | Yes, starting at age 73 | Yes, starting at age 73 | No |

| Most advantageous | When offered by a current employer, especially when a company match is available | When income is high and you expect taxes to be lower in the future | When income is below the limit and taxes are lower today than in the future |

All data is relevant for the 2023 tax year.

*Some employers may administer a Roth IRA.

#Consult a tax professional to discuss your individual situation.+High-income earners may not be able to max out their contributions. This is due to an ERISA regulation that requires testing to ensure that the plan isn't considered too "top-heavy."

Your choices are not necessarily mutually exclusive

We just spent a lot of time explaining the similarities and differences among these various retirement investment vehicles. But in practice, they’re not mutually exclusive. You can potentially invest in all three at the same time. But if you do, the available tax benefit may be lower or not available in the year you make the contribution. And whether you have just one or multiple IRAs, your total annual contribution is still capped at $6,500 ($7,500 over age 50). There are other rules, so consult with a tax professional to understand the impact on your situation.

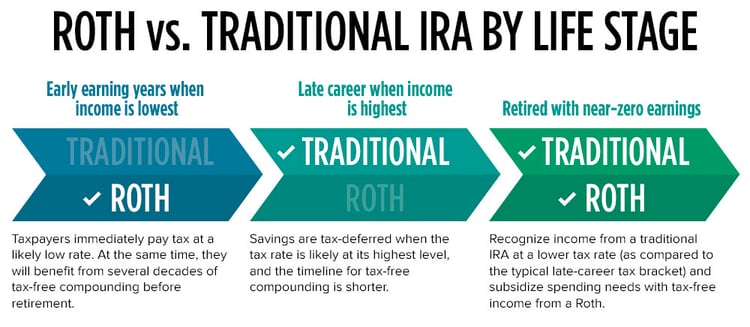

In general, we believe you should start with a 401(k) if available. And if you are able, max out your contributions and take advantage of any company match program. Then consider an IRA. Not sure which makes sense for you? This chart may help.

There are also ways to shift assets from one type of account to another. When you leave an employer, you may want to roll over your 401(k) into your new 401(k) if allowed or to an IRA to consolidate your assets. Or you may contribute to a traditional IRA, then convert it to a Roth via a “backdoor” conversion. There are many advantages to doing these financial maneuvers.

There are also ways to shift assets from one type of account to another. When you leave an employer, you may want to roll over your 401(k) into your new 401(k) if allowed or to an IRA to consolidate your assets. Or you may contribute to a traditional IRA, then convert it to a Roth via a “backdoor” conversion. There are many advantages to doing these financial maneuvers.

With that said, we think the most crucial takeaway from this discussion is one simple word: Save. And start early. Sure, you will likely make more money later in your career, but you also will have more expenses. If you make delaying saving “okay,” you may never get around to saving seriously for retirement.

And the longer you wait, the less time there is for compound growth to multiply your contributions. (Remember the effects of compounding with the employer match we discussed above?) So, your retirement account at retirement will be composed mostly of your contributions rather than the growth your contributions could generate. This loss of compounding is often irreplaceable. So give yourself the gift of time and let the market potentially work for you!

Related Articles

What’s the Difference Between After-Tax and Roth Account Contributions?

Whether you’ve recently started contributing to a 401(k) or you’re a seasoned saver, you’ve...

Traditional IRA vs. Roth IRA: Which is the Best Choice for You?

It’s that time of year when people begin thinking about taxes and investments. How should you...

RMDs Are Mandatory, But Here’s What You Can Control

You must start withdrawing from tax-deferred retirement accounts at a certain age, but there are a...